The London Insurance Market is a distinct and separate part of the UK insurance and reinsurance industry centred in the City of London, predominantly within the EC2 and EC3 postal districts. Its main participants are insurance and reinsurance companies, Lloyd’s of London syndicates, Coverholders/Agents/MGAs, and brokers who handle most of the business.

The London Market has a heritage tracing back to the 17th century and today it is the largest global hub for commercial and specialty risk delivering solutions for risks in almost every territory around the world.

The UK Regulators for the insurance industry are the Prudential Regulatory Authority (PRA) and the Financial Conduct Authority (FCA). The PRA is part of the Bank of England and promotes the safety and soundness of insurers, and the protection of policyholders. The FCA regulates how these firms behave, as well as more broadly the integrity of the UK’s financial markets.

Generally, insurers, including Lloyd’s Managing Agents, are authorised and regulated by both the PRA and the FCA (Dual Regulation). In addition, Lloyd’s of London may be seen as a ‘third regulator’ for its Managing Agents in that syndicate groups must adhere to Lloyd’s Minimum Standards and the Corporation of Lloyd’s Byelaws.

Risk and Control environment – insurance company X

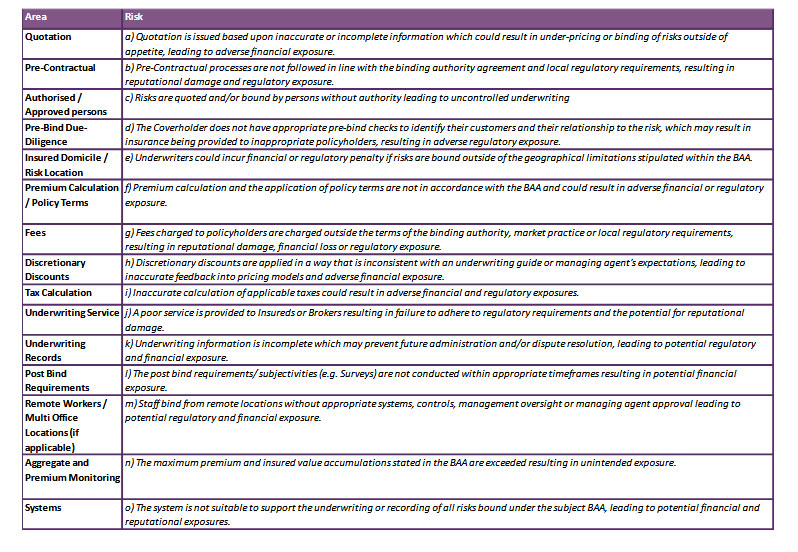

Risk & Control Matrix – Extract. A generic example is shown at Risk & Control Matrix – Underwriting

Audit tools

Lloyd’s Minimum Standards

Lloyd’s Minimum Standards are statements of business conduct which Lloyd’s Managing Agents are expected to comply with to operate at Lloyd’s. LMS can be aligned with the internal control environment and incorporated into an internal audit program. LMS is also a useful tool for company market insurers, and their internal auditors, given its comprehensive reach and contemporaneous character (the current LMS were all updated in January 2021). Under ‘MS2 – Underwriting and Controls’, INSURANCE RISK has two elements “(i) Underwriting risk that insurance premiums will not be sufficient to cover future insurance losses and associated expenses. Underwriting risk also encompasses people, process and system risks directly related to underwriting. (ii) Reserving risk that reserves set in respect of insurance claim losses are ultimately insufficient to fully settle these claims and associated expenses”. MS2 details the ‘effective systems and controls’ expected to mitigate Insurance Risk to levels in line with the insurance company or Lloyd’s Syndicate risk appetite.

Controls sit under two headings:

- Prevent controls – These include, for example, written authorisation and proactive management of each underwriter’s authority and referral processes outside of authority.

- Detect controls – These include, for example, peer review processes and Management Information and exception reporting.

The LMS can be viewed at MS2 Underwriting and Controls

London Market Coverholder Audit Scope

A standard audit scope has been compiled by Lloyd’s with the intention of improving consistency of audits and to assist insurers and coverholders in meeting the expectations of the Financial Conduct Authority (FCA) and in the case of insurers, the Prudential Regulation Authority (PRA). A copy of the scope can be viewed at London Market Coverholder Audit Scope

The key control areas are represented in the following table:

If you need assistance with any aspect of your internal or delegated auditing service offering, JCBFL can help.